Continue advancing in Dynamic Stochastic General Equilibrium (DSGE) modeling with our comprehensive package. Dive into the practical application of the New Keynesian DSGE model with Stata, featuring essential resources such as slides, datasets, a mathematical model book, Stata DO File, and two explanatory videos.

Led by Juan D'Amico, an experienced economist with profound expertise in modeling and Stata, this package delves into the practical implementation of macroeconomic theory outlined in Carl Walsh's renowned book "Monetary Theory and Policy."

While we won't manually solve the equations (the step-by-step derivation is covered in Walsh's textbook, with relevant chapters included in the course materials), we will thoroughly analyze each equation, dissecting how variables and parameters interact.

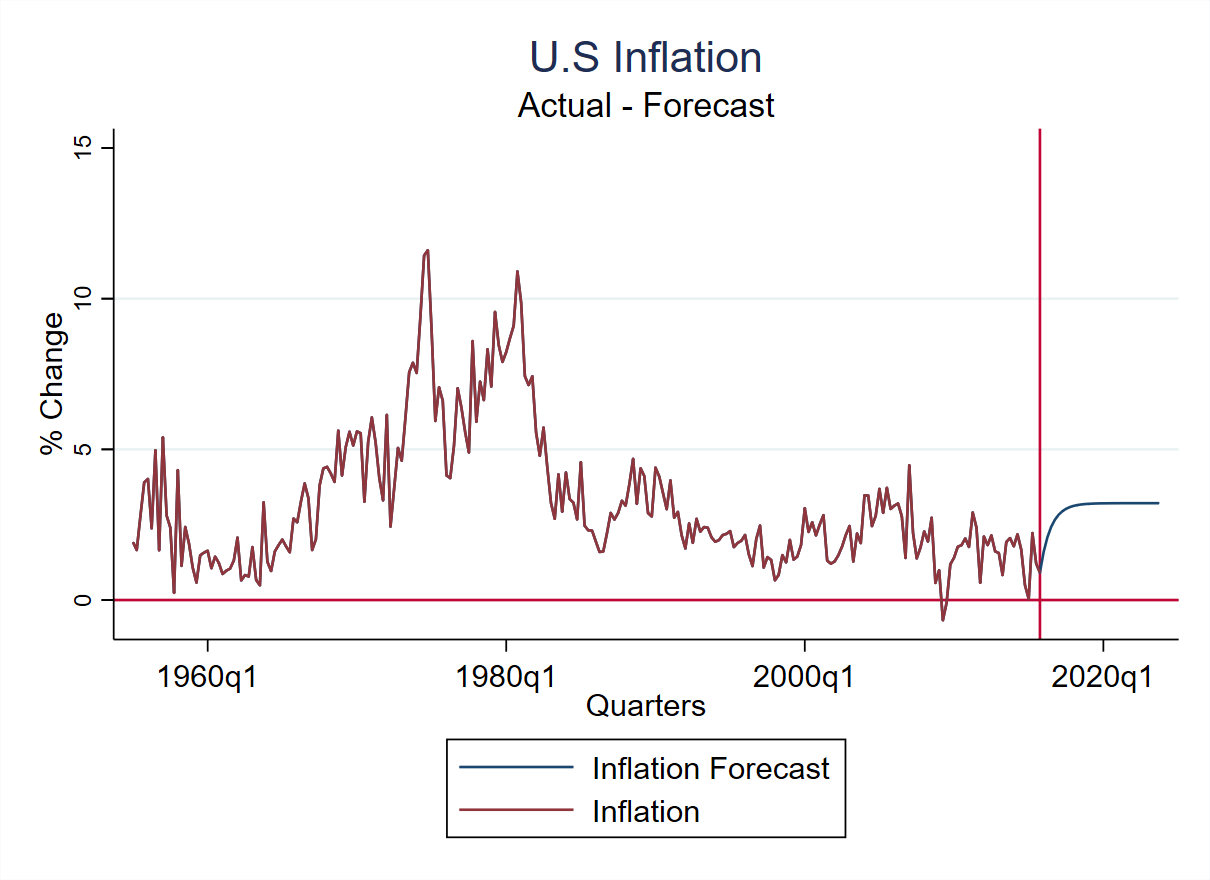

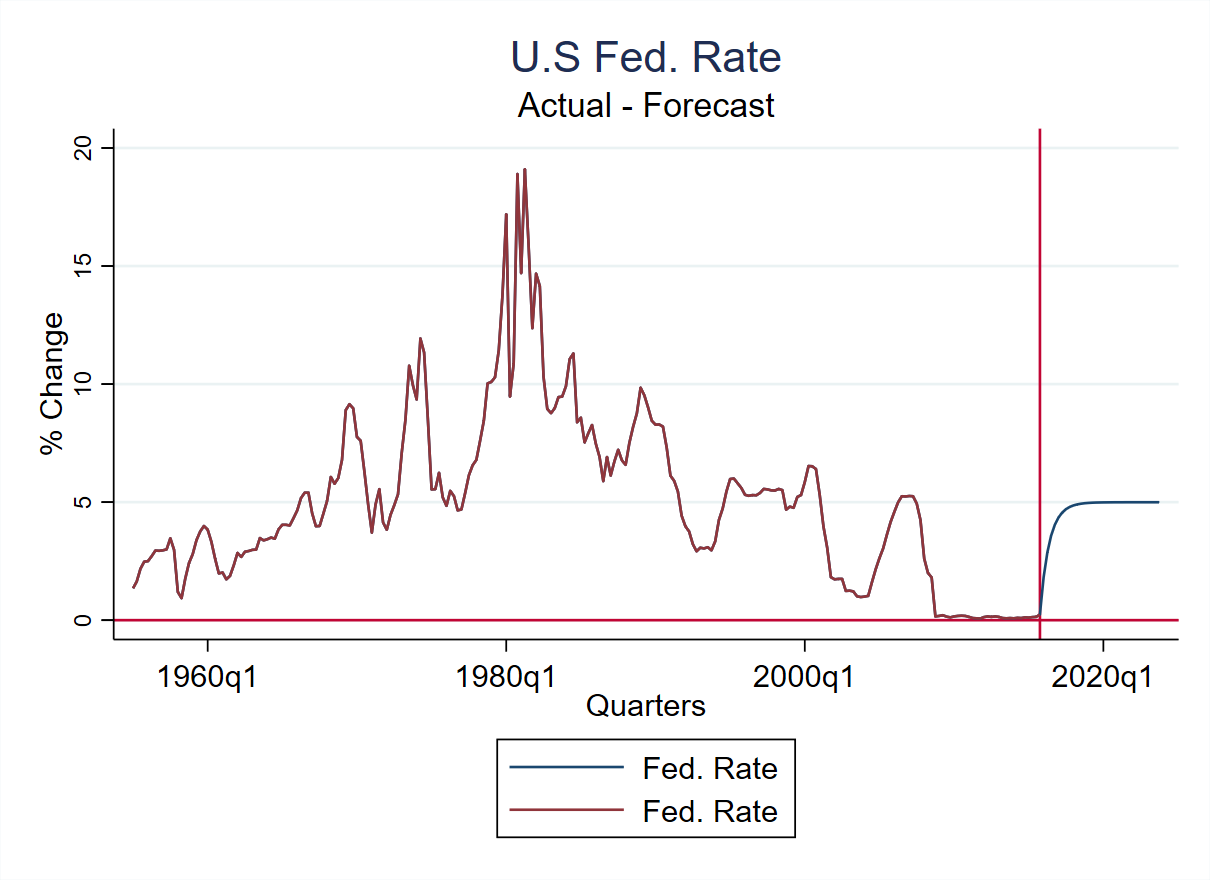

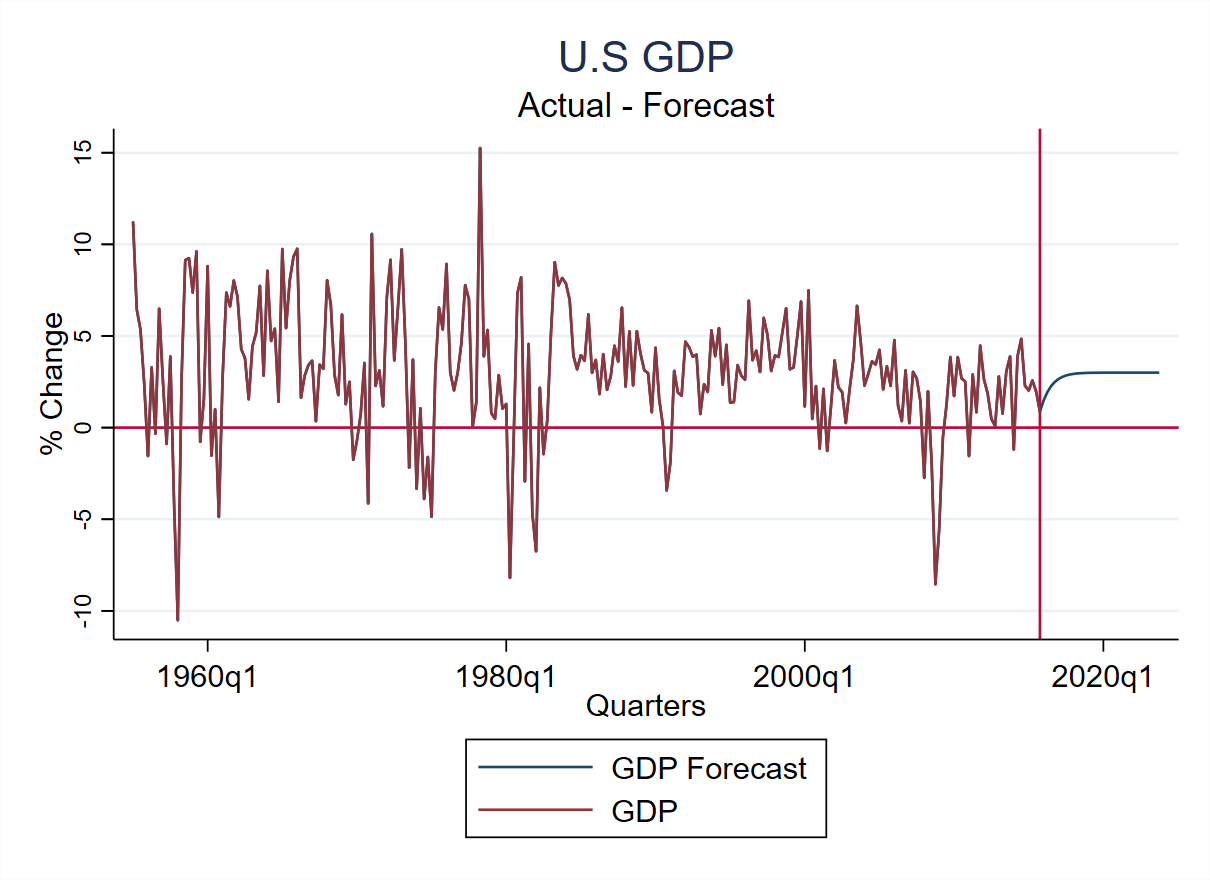

Through these resources, you'll learn to translate these equations into Stata code, produce impulse response functions, and generate out-of-sample forecasts.

Key topics covered include:

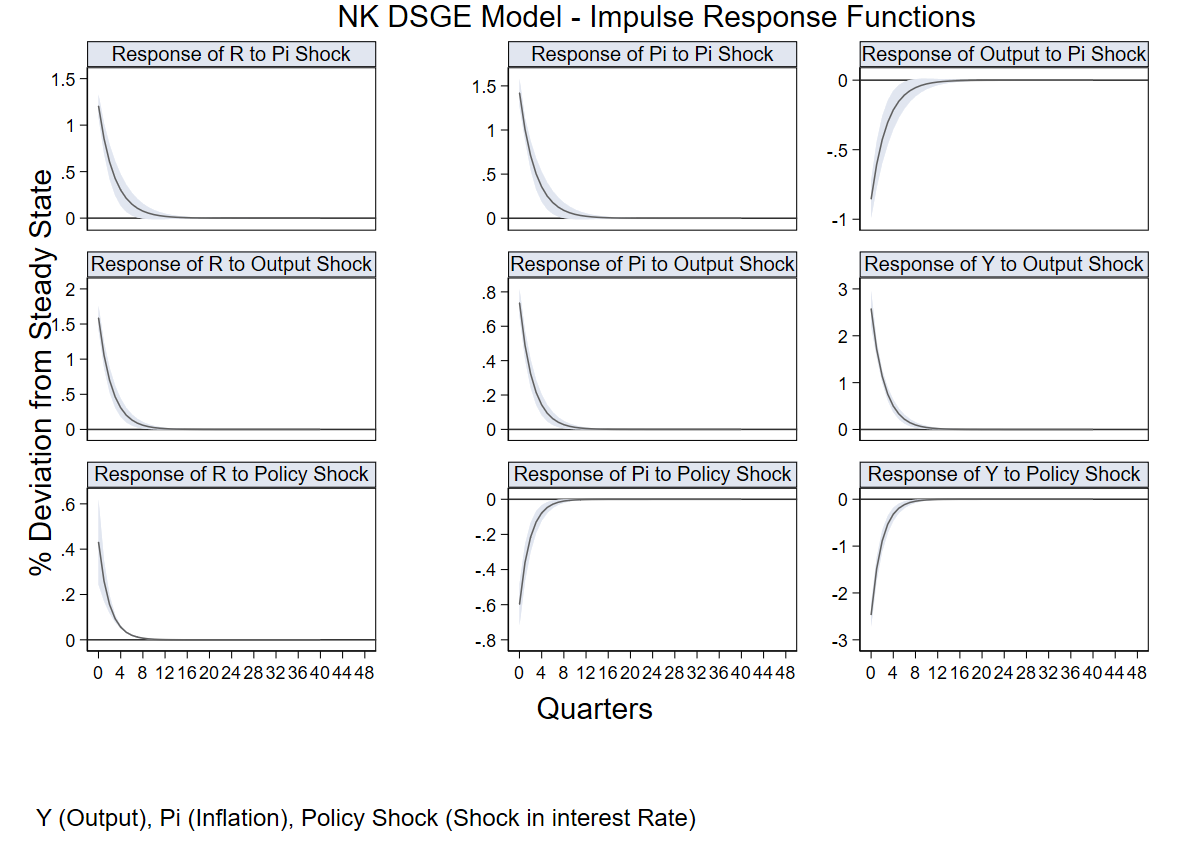

- Understanding the three equations of the New Keynesian DSGE model and their implications for macroeconomic analysis.

- Writing equations in Stata and interpreting the effects of variables and parameters on the model.

- Generating impulse response functions to analyze dynamic responses to shocks.

- Producing out-of-sample forecasts to assess model performance.

- Calibration techniques and parameter estimation to fine-tune the model to real-world data.

Whether you're a researcher, economist, or student, this package offers invaluable insights and practical skills to advance your proficiency in macroeconomic modeling using Stata.

Don't miss this opportunity to enhance your expertise and unlock the full potential of the New Keynesian DSGE model in Stata. Get your package now!