VAR Model EViews - EViews Workfile + Slides + Dataset

On Sale

$4.99

$4.99

This package contains all the material covered in my TWO YouTube Video "How to estimate and interpret VAR models in Eviews - Vector Autoregression model" and "Impulse response function and Variance decomposition - VAR model in Eviews".

The package includes:

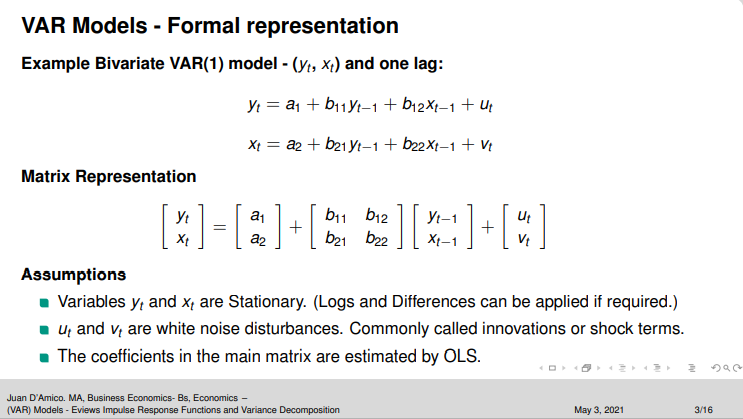

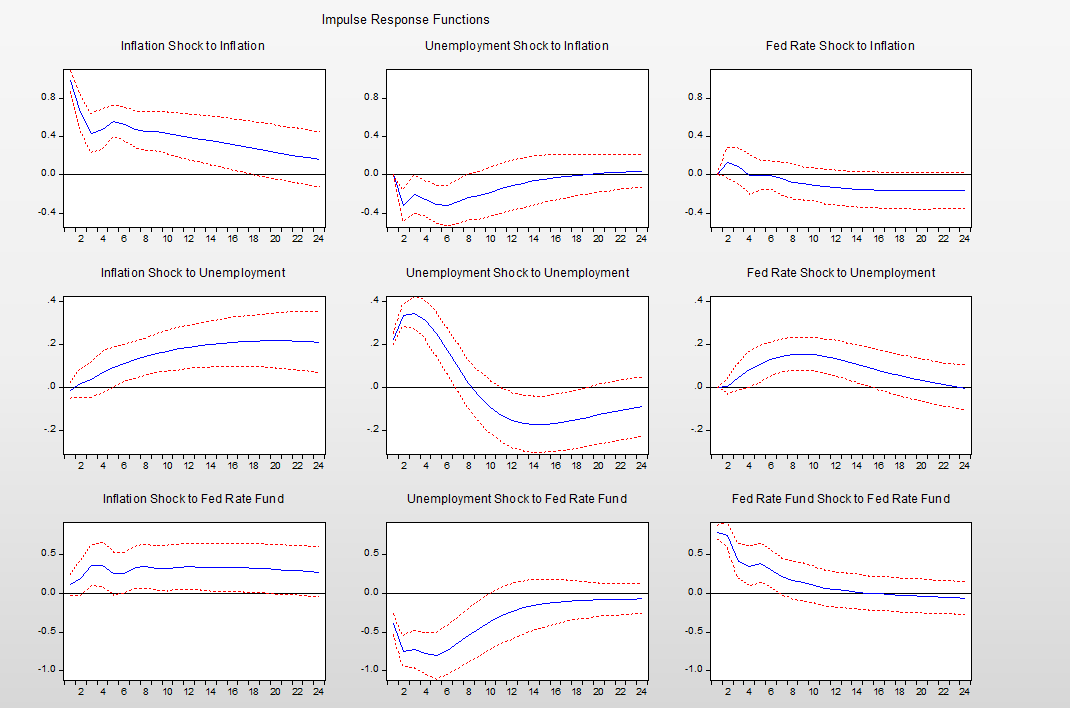

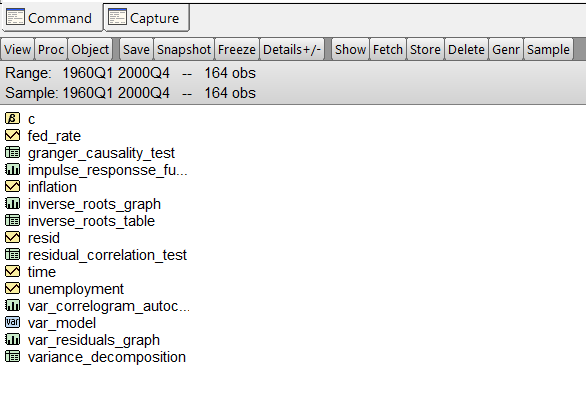

1-EViews Workfile with all the tests, graphs, Impulse response functions, variance decomposition, etc.

2-Video Slides of the TWO videos

3-Data Set

I hope you enjoy it!

JD Economics.

The package includes:

1-EViews Workfile with all the tests, graphs, Impulse response functions, variance decomposition, etc.

2-Video Slides of the TWO videos

3-Data Set

I hope you enjoy it!

JD Economics.